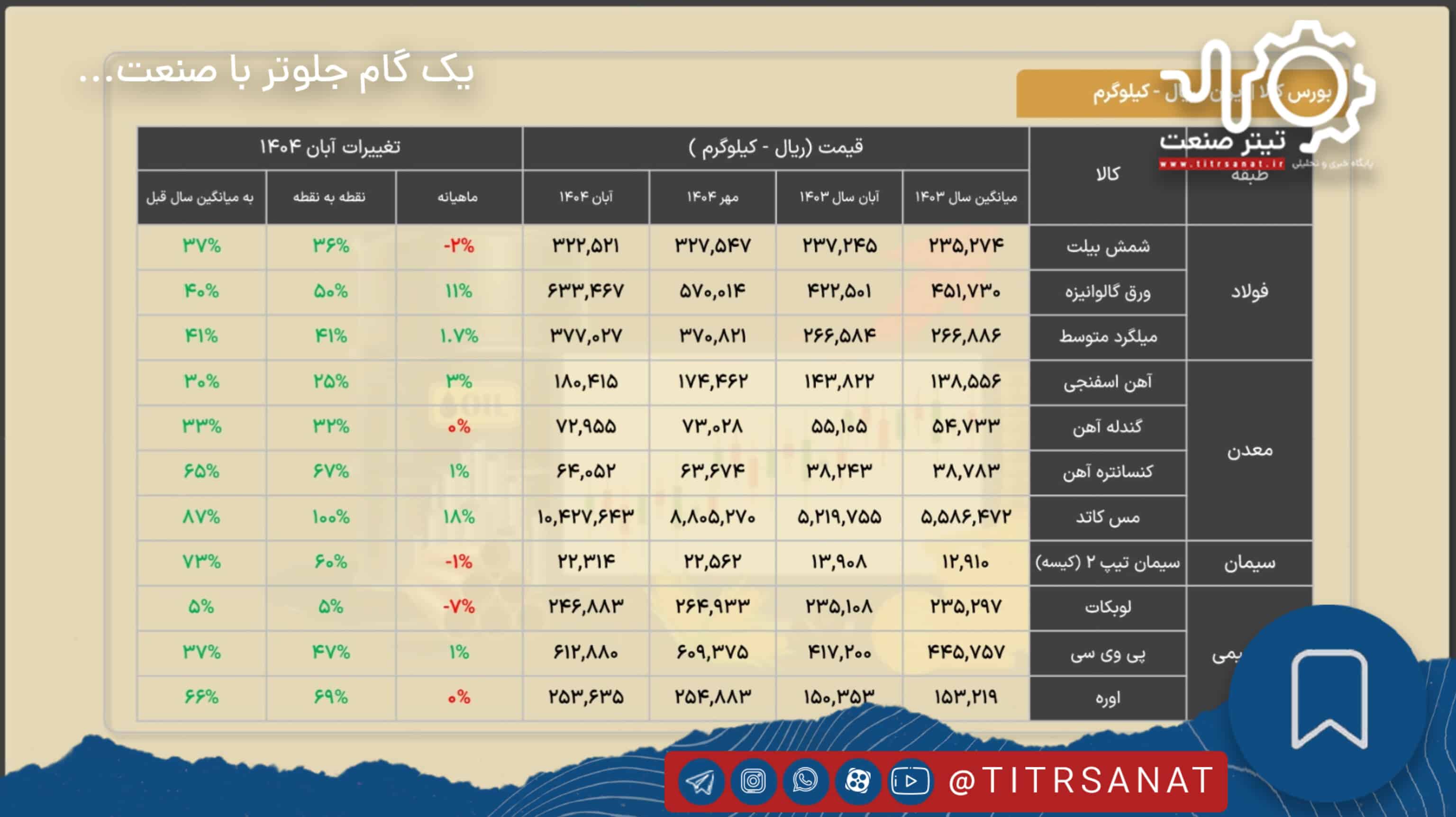

According to Titrsanat, Iran Mercantile Exchange (IME) in Aban 1404 (October–November 2025) presents a mixed picture of growth and volatility across four industrial sub-sectors, including steel, mining, cement, and petrochemicals. In this landscape, currency exchange rate surges, global price fluctuations, and domestic policies have shaped the primary direction of industrial price trends. Meanwhile, copper, with an approximate 18% month-on-month increase and a 100% year-on-year surge, emerged as the most volatile commodity in the industrial price table.

Steel Industry: Between Construction Slowdown and Currency Inflation

In the steel segment, billets as well as flat and long products, following a period of demand stagnation in 1403 (2024–2025), were driven more in Aban 1404 by rising exchange rates and higher energy costs. As a result, part of the real decline in demand has been offset by nominal price increases, which is reflected in the data as positive year-on-year growth. Temporary supply constraints, regulatory policies within the Iran Mercantile Exchange, changes in pricing formulas based on export billet benchmarks, and unstable exports to markets such as Iraq and Afghanistan are among the key factors intensifying volatility in this segment.

Mining Industry: Responding to Global Markets and Export Policies

In the mining sub-sector, products such as iron ore, concentrate, and pellets experienced limited growth in 1403 (2024–2025), in line with the temporary decline in global iron ore prices and pressure on steelmakers’ profit margins. However, in Aban 1404, with the partial recovery of global prices and a sharp rise in exchange rates, the overall direction of the figures in the table turned upward. The imposition and adjustment of export duties, constraints in rail and maritime transportation, changes in the terms of long-term contracts between mines and steel producers, as well as investment and safety risks in mining operations, are assessed as key drivers of price level changes in this sector.

Cement Industry: Volatility Under the Shadow of Energy Constraints and Construction Slowdown

The cement market in 1403 (2024–2025) was caught between two opposing pressures: on the one hand, a construction slowdown and a real decline in demand, and on the other, successive increases in fuel and transportation costs, which in some months led to price growth despite weak demand. In Aban 1404, the partial liberalization of pricing on the Iran Mercantile Exchange, the persistence of high energy costs, and changes in freight rates—particularly on export routes to Iraq and Afghanistan—resulted in notable year-on-year increases in several rows of the table, although on a month-on-month basis, negative or neutral fluctuations are also observed for some products.

Petrochemical Industry: Sensitive to Feedstock Costs and Global Prices

In the petrochemical sector, products such as urea and certain solvents or lube cuts are directly affected by global price fluctuations and changes in gas feedstock pricing formulas. This impact is clearly reflected in the month-on-month and year-on-year variations shown in the Aban 1404 data table. Export restrictions, conditions in the global fertilizer and polymer markets, maritime freight rates, and foreign exchange repatriation policies for export revenues have determined the main direction of price movements, leading to double-digit growth in some items while resulting in declines or stability in others.

Copper at the Center of Investors’ Attention

Across the overall market, copper—recording both the highest month-on-month growth and the largest year-on-year increase—has emerged as a symbol of the intensified impact of global and currency variables on Iran’s strategic commodities in Aban 1404. This surge can be traced to global supply shortages, rising prices on international exchanges, and the sharp increase in exchange rates.

By contrast, commodities that have shown only limited growth in the table despite broad inflationary pressures are largely victims of a combination of weak domestic demand, market regulation policies, and excess capacity. This sends a clear signal to policymakers and market participants alike regarding the need to redesign pricing models and expand exports in the coming years.

Comments